Recently, as I listen to the growing chorus of investors claiming that U.S. Treasury yields are poised to rise and return to their historical norm, I am reminded of a Keynesian sentiment about the problem with long-term thinking. Last week, for example, I was at a meeting of prominent investors where nearly everyone held the view that rates must normalize. I sat there listening, and thought, "Normalize to what?" As my fellow investors shared forecasts for forward rates and everything else, at one point I remarked that people are flattering the Federal Reserve, giving it too much credit for why long-term interest rates are where they are today.

What I mean by this is that when I look around the world and consider what is going on, it is hard to argue that U.S. 10-year Treasuries with yields hovering near 2.5 percent are unattractive compared to 10-year Japanese government bonds yielding close to 50 basis points. German 10-year bunds are yielding a historic low of just over 1 percent with the Treasury/bund spread as wide as ever. Even in troubled Spain, benchmark borrowing costs in recent days have at times dipped below 2.5 percent -- their lowest yield since 1789. Add to that the perception that both the yen and euro are seemingly a one-way bet toward depreciation and it is reasonable to expect that international capital will continue flowing toward the United States, pressuring U.S. Treasury yields down as quantitative easing draws to an end.

Most investors can agree that loose monetary policy and quantitative easing have caused overvaluation in some spheres of U.S. credit. Even Federal Reserve Chair Janet Yellen has said that some leveraged credit is showing signs of frothiness. But the palpable fear that the Fed’s eventual hiking of short-term interest rates will prompt a general upward shock in interest rates and an abrupt repricing of credit risk and U.S. Treasuries is getting overplayed and too much attention. The reality is that with international demand for U.S. Treasuries likely to increase and the size of incremental U.S. government borrowing expected to decline because of shrinking federal budget deficits, U.S. Treasury yields could move lower.

The likelihood that we are going to have a sudden, ugly increase in interest rates seems fairly remote for now. As for the long-run, well, the consensus view of interest rates normalizing will eventually come true. The problem with that thinking may lie in the definition of "long-run." As John Maynard Keynes wrote in "A Tract on Monetary Reform" in 1923, "In the long-run we are all dead."

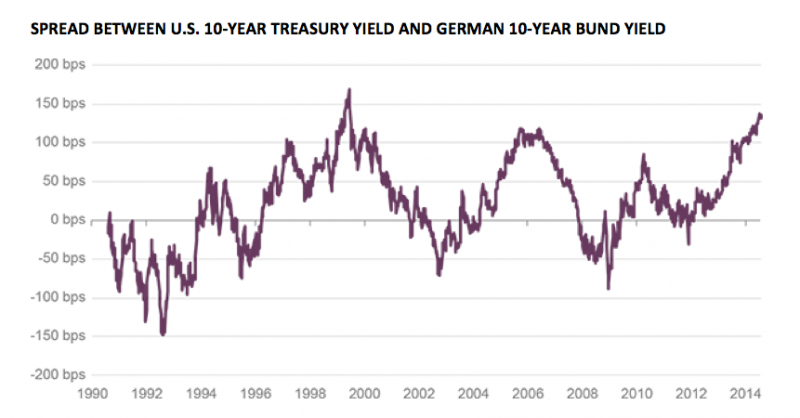

History Suggests U.S. Treasury-Bund Spread May Tighten

It is hard to argue that U.S. Treasuries are overvalued with yields around 2.5 percent compared to German 10-year bunds yielding near historic lows just above 1 percent. The spread between Treasuries and German bund yields, at 138 basis points, is rapidly approaching record levels. The last two times the spread was so wide it soon reversed course. Unless bund yields head higher, unlikely given accommodative ECB monetary policy, Treasury yields could fall in the near term.

{kind=link}

Source: Bloomberg, Guggenheim Investments. Data as of 7/30/2014.

This material is distributed for informational purposes only and should not be considered as investing advice or a recommendation of any particular security, strategy or investment product. This article contains opinions of the author but not necessarily those of Guggenheim Partners or its subsidiaries. The author’s opinions are subject to change without notice. Forward looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission of Guggenheim Partners, LLC. ©2014, Guggenheim Partners. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information.

Scott Minerd is Chairman of Investments and Global Chief Investment Officer at Guggenheim Partners